How to Become a Financial Life Coach: Your 2026 Guide

Coachful

You might be standing at your kitchen counter with a color-coded budget, a stack of books on behavior change, and a question you haven't said out loud yet. Could I do this for a living? Not just help friends with a spreadsheet, but guide people through the fear, shame, avoidance, and conflict that money brings up.

That question usually appears alongside another one. What if I'm good with my own money, but not qualified to help someone else with theirs? That's the right concern to have. It means you're taking the work seriously.

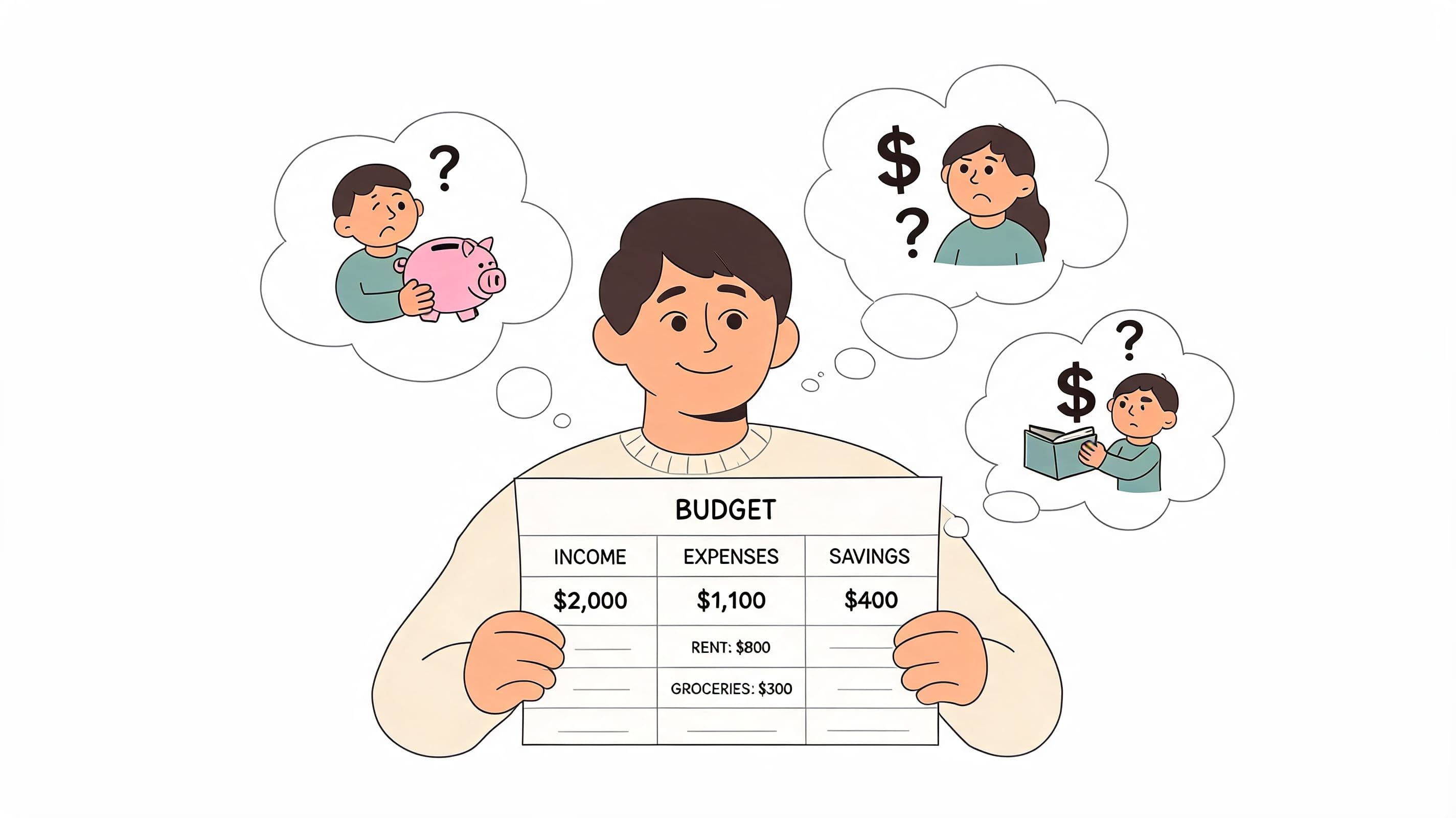

How to become a financial life coach isn't really a question about money first. It's a question about role. You are moving from being the organized one in your circle to becoming a practitioner who can hold space, ask sharp questions, set boundaries, structure change, and build a business around that skill. The numbers matter. The budget matters. But people rarely stay stuck because they can't add.

They stay stuck because they avoid, freeze, overspend to self-soothe, undercharge, fight with a partner, or feel guilty every time they spend on themselves. A financial life coach works in that territory. If that sounds meaningful to you, you're looking at a career with real momentum. The global coaching industry generated $5.34 billion in revenue in 2025, with projections of $5.8 billion by 2026, and in the US, financial coaches earn an average annual salary of $73,423, according to Life Purpose Institute's coaching industry outlook.

Beyond Spreadsheets Are You a Coach or Just Good with Money

Being good with money is useful. It is not the same as being a coach.

A financial advisor typically works with financial products and investment recommendations. A financial planner usually handles broader planning problems such as retirement, tax-aware strategy, and asset allocation. A financial life coach helps clients change the way they think, feel, and behave around money so they can make better decisions consistently.

That difference matters because many new coaches make the same mistake. They assume clients are hiring them for answers. Most clients are hiring you for clarity, accountability, and calm.

What the work actually looks like

A client says, "I know I should stop spending on takeout, but every bad day ends the same way." If you are just good with money, you say, "Set a dining budget and delete the apps."

If you are coaching, you go deeper.

You might ask:

- Pattern first: "What usually happens right before you order?"

- Emotion next: "What feeling are you trying to escape or create?"

- Meaning check: "When you spend in that moment, what does it give you besides food?"

- Behavior design: "What's a smaller replacement you would realistically do on a hard day?"

That conversation produces a different result. The client doesn't just leave with a tighter budget. They leave with insight into their own behavior and a plan they can realistically follow.

Practical rule: If your instinct is to solve too quickly, slow down. Coaching starts where advice alone stops working.

The shift from fixer to guide

People new to this field often worry that they need to know everything. They don't. They do need to know what belongs in coaching and what belongs elsewhere.

Your role includes:

Helping clients name the core problem "I'm bad with money" often means "I avoid looking at my accounts because I feel ashamed."

Turning vague stress into concrete goals

"I want to feel better" becomes "I want to stop overdrafting, build a simple spending plan, and talk to my partner without shutting down."Creating accountability without judgment

You are not a scolding parent. You are not a rescue worker. You are a steady mirror with structure.

A simple example. A client comes in carrying guilt about spending on their kids while also falling behind on bills. The obvious move is to cut spending categories. The coaching move is to explore the story underneath it. Maybe they equate good parenting with always saying yes. Maybe deprivation from childhood is driving overcompensation now. Once that pattern is visible, budgeting starts to work because the client stops fighting an invisible emotional script.

The strongest financial life coaches aren't the ones with the fanciest spreadsheets. They're the ones who can help a client tell the truth about their money behavior without collapsing into shame.

If you're reading this and thinking, "That sounds more human than financial," that's exactly right.

Building Your Foundation with Skills and Certifications

Imposter syndrome usually shows up early. "I don't have formal training." "I've only managed my own money." "What if someone asks a question I can't answer?"

The answer is not to pretend confidence. The answer is to build a real foundation.

Two skill sets matter

You need enough financial literacy to help clients with everyday money decisions, and enough coaching skill to help them follow through.

Your financial base should cover topics such as:

- Cash flow and budgeting: helping clients see where money is going and make intentional trade-offs

- Debt decisions: understanding common pathways clients consider, including budgeting changes, repayment prioritization, and educational resources on debt consolidation and settlement when someone is exploring debt relief options

- Saving habits: emergency funds, goal-based saving, and basic spending boundaries

Your coaching base should include:

- Active listening: hearing the belief underneath the numbers

- Questioning: asking what opens reflection instead of provoking defensiveness

- Goal setting: turning emotional overwhelm into small, trackable commitments

A coach who knows money but can't coach often overwhelms clients. A coach who can listen well but lacks financial grounding can leave clients encouraged but directionless. You need both.

Why certification helps

Certification isn't legally required. It is still one of the best ways to become competent faster and feel less shaky in front of clients.

According to the NFEC, certifications such as the CPFC provide structured preparation, and the CPFC includes a 180-hour program. Credentials from AFCPE also give coaches grounding in coaching techniques and regulatory compliance. The practical value is simple. Good training helps you stand out, build trust, and move from theory to client management, as described in the NFEC overview of becoming a financial life coach.

How to choose without overcomplicating it

Pick a certification based on the work you want to do, not the initials you want after your name.

Consider these questions:

- Do you want strong teaching structure? Programs like CPFC are useful if you want a guided curriculum and formal training hours.

- Do you want broader counseling credibility? AFCPE-related pathways can appeal to people who want a strong client education and guidance foundation.

- Do you need to start before everything is perfect? Then choose a program you can complete while beginning supervised practice, peer practice, or volunteer coaching.

One mistake I see a lot is endless credential shopping. Someone spends months comparing programs, reading forums, and waiting to feel "ready." Meanwhile, they still haven't coached a single human being.

Certification should reduce hesitation, not become a sophisticated form of avoidance.

What to do while you train

Don't wait for a certificate to begin developing coach behavior. Practice in low-risk settings.

Try this:

- Run practice sessions: coach a peer through one money habit issue, not their entire financial life

- Document your questions: notice which questions create clarity and which sound clever but go nowhere

- Study strong coach behavior: Coachful's guide on coaching traits is a useful benchmark for the interpersonal side of the work

The fastest confidence builder is not more theory. It's doing the work in a structured way, reflecting on it, and improving.

Designing Your Services and Setting Your Price

A new financial life coach often asks the wrong pricing question. They ask, "What should I charge per hour?" A better question is, "What transformation am I helping a client achieve, and what structure gives them the best chance of getting there?"

If you charge only by the hour, you train clients to compare you to a conversation. What you are really selling is a process.

Start with outcomes, not session counts

Most clients don't want six sessions. They want relief. They want a plan. They want fewer money fights. They want to stop avoiding their banking app. Build offers around that.

Here are three examples.

90-Day Financial Reset

This works well for a young professional living paycheck to paycheck despite a solid income. You might include an intake assessment, a spending review, goal setting, regular coaching sessions, between-session accountability, and a simple action plan.

Couples Money Harmony

This suits couples who keep having the same argument in different forms. One partner spends freely, the other tightens everything. The package can include shared values work, a money meeting framework, conflict scripts, and decision rules for joint spending.

Debt Recovery Coaching Program

This is for clients carrying shame and confusion around debt. The offer may focus on triage, spending stabilization, emotional triggers, debt-priority planning, and accountability around behavior change.

Choosing Your Financial Coaching Pricing Model

| Model | Best For | Pros | Cons |

|---|---|---|---|

| Hourly sessions | Very early-stage coaches testing demand | Easy to explain, simple to start | Rewards fragmentation, can make clients hesitate to book |

| Package pricing | Coaches solving a specific client problem | Clear transformation, stronger commitment, easier planning | Takes more thought to design well |

| Monthly retainer | Ongoing accountability support | Predictable revenue, steady client contact | Can feel vague if scope isn't defined |

| Group program | Coaches serving a shared audience such as debt recovery or money mindset clients | Better leverage, peer accountability, scalable delivery | Needs structure, facilitation skill, and stronger systems |

How to set a price without apologizing

The coaching market includes practitioners with strong earning potential. Experienced practitioners often charge $100 to $150 per hour, and top executive coaches can charge more, according to this summary of coaching income and pricing data. That doesn't mean you should copy someone else's rate blindly. It does mean you shouldn't assume low pricing is the only ethical option.

Price based on three factors:

- Problem severity: solving chronic debt panic is not the same as helping someone tidy a budget

- Support level: access between sessions, reviews, worksheets, and accountability all increase value

- Client commitment: a serious transformation usually needs a defined container, not one-off chats

A common beginner move is underpricing because it feels safer. It rarely is. Low prices attract hesitant clients, create resentment, and make it hard to deliver focused attention.

If a client says yes quickly because your price feels tiny, that isn't always market validation. Sometimes it's a sign your offer sounds disposable.

Try writing your offer in plain language. "I help couples stop recurring money conflict and create a shared system they can stick to." That is easier to price than "I do financial coaching sessions."

When clients can see the before and after, pricing gets easier for both of you.

Launching Your Business and Finding Your First Clients

The business side feels bigger than it is. You do not need a brand agency, a full funnel, or a polished social presence before you begin. You need a credible basic setup and a repeatable way to start conversations.

Start with the minimum professional layer: a business name you can live with, a simple coaching agreement, a payment method, a booking process, and a short website. If you don't want to wrestle with design, use tools that help you build a coaching website without turning the project into a second career.

How the first three clients often happen

Client one usually comes from your existing network, but not because you post, "I'm open for business" and wait. It comes from a direct, respectful message.

For example: "I've started a financial life coaching practice focused on helping people reduce money stress and build practical habits. If someone comes to mind who feels stuck around spending, debt, or money communication, I'd appreciate an introduction."

That message works because it names the problem. It doesn't ask people to guess what you do.

Client two often comes from a small event. A new coach might offer a free workshop at a local coworking space, community group, or online meetup. The topic matters. "Budget Better" is bland. "Why Smart People Still Avoid Their Money" is specific and psychologically accurate.

After the session, one person stays behind and says, "This felt uncomfortably familiar." That's your lead.

Simple marketing that doesn't feel fake

The coaches who find early traction usually do a few grounded things well.

- Teach a narrow topic: one short webinar on spending triggers, couples money meetings, or getting unstuck from debt shame

- Write where your audience already pays attention: a guest post for a personal finance site, local newsletter, or niche community

- Use conversations, not performance: private outreach beats broadcasting when you're new

If you want help thinking more practically about visibility and small-business outreach, NineArchs' insights for SME growth offer useful perspective on how small operators can approach marketing without trying to look like a large company.

Here is a useful mindset reset before you market.

You are not persuading strangers to want something they don't need. You are helping the right people recognize a problem they've already been carrying.

A short explainer can also do a lot of heavy lifting when you're trying to clarify your offer and process for prospects.

What a clean first month can look like

Week one, you finalize your offer and website. Week two, you invite people into a free talk or Q and A. Week three, you follow up with attendees who replied, asked questions, or lingered after the event. Week four, you convert one or two into paid discovery calls.

This is not glamorous. It is effective.

The main thing that does not work is hiding behind preparation. New coaches tell themselves they need better branding, another certification, or more content before reaching out. Usually they need ten honest conversations.

Systematizing Your Practice for Growth and Sanity

Most new coaches expect the hard part to be coaching. It usually isn't. The hard part is the mess around coaching.

You finish a strong session, then spend the next hour chasing an invoice, rescheduling next week's call, digging through notes, and trying to remember whether the client committed to a spending pause or a debt review. That friction adds up fast.

Why manual systems break first

A common challenge for many capable coaches is stalling. A 2025 ICF Global Coaching Study found that 62% of independent coaches cite time lost to admin as their top barrier to growth, and the same verified data notes that tech adopters scale 2.5x faster, as summarized in Indeed's career guide on becoming a financial coach.

That finding tracks with what happens in practice. Manual tools seem cheap at first. A spreadsheet here, separate calendar there, invoices in another app, session notes in a document folder. Then clients increase, details scatter, and your attention gets pulled away from the actual work.

The minimum systems worth setting up early

You do not need a giant operations stack. You do need a small set of repeatable workflows.

Use a simple checklist:

- Client onboarding: intake form, agreement, payment setup, first-session prep

- Session management: booking, reminders, notes, and follow-up actions in one place

- Progress tracking: goals, milestones, and wins captured consistently

- Financial admin: invoices, payment records, and clean documentation

If you're operating as a solo business, clean records matter more than most coaches realize. For a practical look at managing records as a UK sole trader, Receipt Router gives a useful breakdown of what to keep organized so admin doesn't become a tax-season panic.

A system doesn't make you less personal. It makes your consistency visible.

Growth gets easier when delivery is structured

There is also a business reason to systematize early. Without structure, every new client creates more complexity. With structure, each new client fits into a working process.

That matters if you want to move beyond one-to-one work. Group coaching, cohorts, guided programs, and structured accountability all depend on repeatable delivery. If every session, reminder, payment, and note lives in a different place, you won't scale with much peace.

A calm coaching business usually looks boring from the outside. The forms are ready. The reminders go out. Notes are easy to find. Clients know what's next. Boring is good here. Boring means your energy stays available for insight, not logistics.

The Art of the Coaching Journey and Measuring True Success

Once a client signs, the core work begins. A good coaching journey has rhythm.

What clients need at each stage

The discovery call is not for impressing them. It is for understanding the problem, naming the fit, and setting honest expectations. If someone wants product recommendations or specialized financial planning beyond your scope, clarity serves them better than trying to stretch your role.

In the first full session, your job is to slow the chaos down. Listen for goals, yes, but also for contradictions. A client says they want freedom, then describes a routine built around guilt and avoidance. That contradiction is often where the work starts.

After that, progress usually comes through a simple pattern:

- Awareness: spotting a money behavior before it fully takes over

- Experimentation: trying one new action that is small enough to repeat

- Accountability: reviewing what happened without drama

- Integration: turning a one-time win into a stable habit

What success actually looks like

Some wins are obvious. A client creates a spending plan. A couple finally holds a calm money meeting. Someone follows through on a debt payoff strategy instead of freezing.

But the deeper success markers are often emotional and behavioral.

A client who no longer feels dread at the grocery checkout has changed something important, even before every financial goal is complete.

Watch for signs like these:

- Increased honesty: they stop hiding purchases or avoiding statements

- Better self-trust: they make decisions without spiraling

- Less shame: they can discuss money without sounding defeated

- More agency: they act sooner and recover faster after setbacks

This is why becoming a financial life coach can be so fulfilling. You are not only helping people organize money. You are helping them rebuild their relationship with choice, responsibility, and hope.

If you're ready to turn your coaching skill into a practice that feels professional from day one, Coachful gives you one place to manage onboarding, scheduling, payments, notes, goals, and client progress without stitching together a pile of separate tools. It's a strong fit for financial life coaches who want less admin clutter and more time doing the work that changes lives.